There is always some confusion among term, whole and universal life insurance. All these insurance types are normally offered by insurance companies and insurance brokers, but how do they differ from each other? We will clarify the differences in this article.

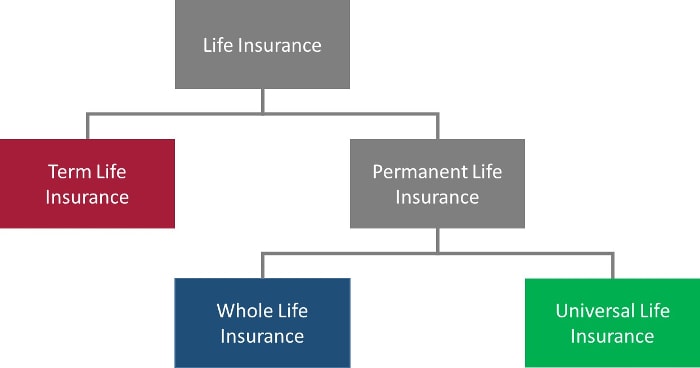

First of all, one needs to understand the overall classification of these insurance types. As per the chart below, there are two basis insurance types, term and permanent, and they are based on coverage length: if coverage is available for a period of time, or until death. Furthermore, permanent insurance can be split into whole life insurance and universal life insurance.

Now we will dive deeper into the difference among these three types of insurance.

Life Insurance Types – Length of Coverage

One of the key differences is how long each policy covers you (or, in insurance words, the “policy term”). For example, Term 20 means that an insurance policy provides coverage for 20 years.

Obviously, the longer is the term, the more expensive will be your term life insurance quote.

Whole life insurance has no end of coverage as long as you pay the premiums. Its main objective is to cover the policyholder for his or her lifespan, and also to accumulate value.

If you need, you can borrow from the accumulated value.

Similar to whole life insurance, universal life insurance is considered a permanent insurance type that covers the policyholder as long as the cost of insurance and policy fee has been paid.

If you need, you can borrow from any accumulated values.

Life Insurance Types – Product Type

In general, insurance products can have two major components: the insurance component that protects the policyholder, and a savings component that accumulates wealth.

Here are the main differences among three insurance products:

This policy type has only one insurance component – it is a purely an insurance product that protects the policyholder and does not accumulate any value. Once the protection period (term) has passed, the policy disappears.

A term life insurance quote is easy to get and this product is the easiest to understand.

Whole life insurance combines both an insurance and a saving component. While insurance protection offers a death benefit once the policyholder dies, the savings component accumulates value that can be used for different purposes.

It is important to know that if you have a whole life insurance policy, an insurer determines where your investment is invested. Interest rates on your investments are typically adjusted annually.

Insurance Rates for different Life Insurance Products

Insurance rates and so life insurance quotes differ from policy to policy and they are strongly driven by product type, but also by the profile of the person getting life insurance (e.g. current health status, family medical history, heath pre-conditions, smoking vs. non-smoking, age, etc.)

If we compare the same insurance policy (meaning the same policy coverage), then the situation looks like the following:

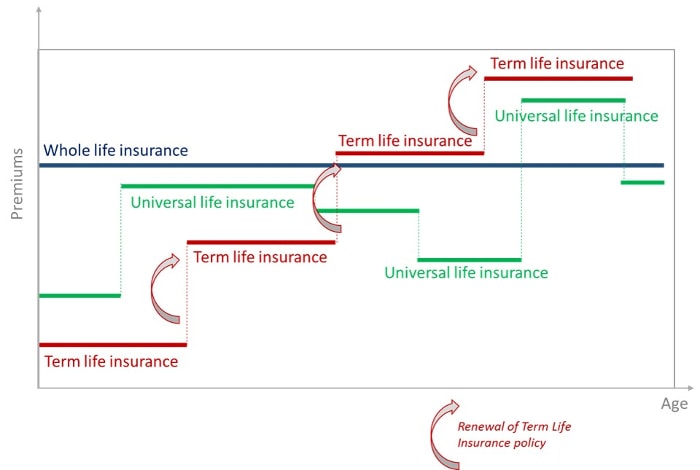

Insurance rates stay the same over the course of your life and they are significantly higher than the premiums one would pay for a comparable term insurance policy with the same coverage. In this case, a whole life insurance quote can be several times more expensive.

It is important to understand, though, that if you later decide to renew your term insurance policy, those premiums might be even higher than whole life insurance premiums (see the chart below).

The chart above shows that at the beginning of your payments (when you are younger), term insurance typically costs less, but the rate goes up with each renewal. You would still have an option to get a term life insurance policy with a renewable option, basically guaranteeing you the rate at each renewal point. This helps you avoid unexpected increases while getting a new term life insurance quote.

Comparing Renewals for Different Life Insurance Products

Given their nature, these products have a very different approach to a policy renewal:

There are actually two options available for you:

- Renew at a standard rate by getting a normal term life insurance quote (it will be higher than the previous rate since life insurance costs go up with age).

- Renew at a predetermined rate that was pre-defined, if you purchased the renewable option of term life insurance.

Similar to whole life insurance, there is no need to renew a policy since it is in place for life and protects you/accumulates cash as long as you pay the insurance premiums.

You can, though, adjust your rate as you want (within pre-defined ranges).

Typical Scenarios for Choosing Each Life Insurance Policy

As these policies are quite different, so are the situations when you should consider getting them.

This policy is best to use when one or more of these scenarios are true:

- You need to cover a short-term risk when you know its duration (e.g. paying off a mortgage, making sure the kids have enough funds for university or college, etc.).

- When you prefer to invest your money on your own, via your advisor or bank instead of letting an insurance company do it for you (“buy insurance, invest the difference”).

This policy is best to use when you have enough money to pay significantly higher premiums (as compared to term life) in the beginning and you do not want to deal with investment choices, letting an insurer to invest for you.If the policyholder dies, family members (other beneficiaries) can use the funds for a variety of reasons, from paying off a mortgage, dealing with existing personal or business debt, etc.

In the end, it is your decision which insurance product you choose, depending on your financial situation and preferences. Many financial specialists (e.g. Suzy Orman), though, tend to keep a clear separation – suggesting you purchase insurance for protection only and let an investment specialist invest the difference between term and permanent insurance.

If you still prefer to get protection for life but are not excited about universal or whole life insurance, look into Term 100 insurance that covers policyholders for life (premiums are paid to age of 100) and typically pays benefits at age 100 if a policyholder is alive.

There are several ways how you can get a no medical term life insurance quote, whole life insurance quote or universal life insurance: through an insurance agent, insurance broker or directly by calling an insurance company (via a call centre). The most advisable way to go is an insurance broker because he/she can compare offers from many insurance companies and find for you’re the best price – get your life insurance quote today and start saving.

{kind=link}