Guaranteed Life Insurance in Canada (No Medical Exam Required)

We specialize in no medical life insurance in Canada and work with over 20 insurers to help you find the right coverage at the right price.

Request your guaranteed life insurance quote — no medical exam required.

Quick Navigation

What is Guaranteed Issue Life Insurance?

Guaranteed issue life insurance (also called guaranteed life insurance) is a type of no medical life insurance policy that you cannot be turned down for, no matter your health.

There are:

- No medical exams

- No health questions

- No risk of being denied

If you meet the age requirements, you’re approved.

This makes guaranteed life insurance in Canada a good option if:

- You have health issues

- You’ve been declined for life insurance before

- You’re a senior and other options are no longer available

It’s designed to give you peace of mind, knowing your loved ones will have financial support when they need it most.

Keep in mind, these policies usually offer smaller coverage amounts (often up to $50,000) and cost more than other types of life insurance.

How Guaranteed Life Insurance Works

Getting guaranteed life insurance in Canada is simple and designed to remove the usual barriers.

Here’s how it works:

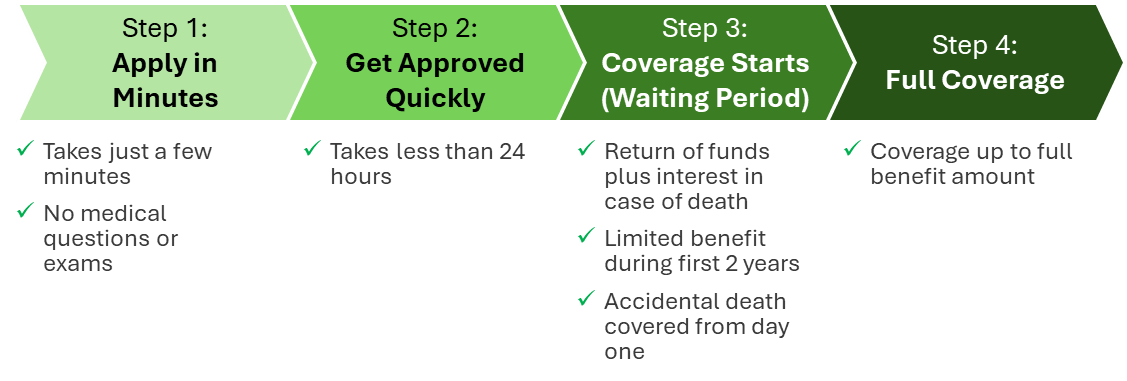

Step 1: Apply in Minutes

Step 1: Apply in Minutes

You complete a short application – there are no medical exams and no health questions.

Step 2: Get Approved Quickly

Because there’s no underwriting, approval is usually instant or within 24 hours.

Step 3: Coverage Starts (Waiting Period)

Once approved, your policy is active and your premiums are locked in. Most policies include a 2-year waiting period for non-accidental death:

- If death occurs during this time, your beneficiaries typically receive a refund of premiums paid, plus interest

- Accidental death is usually covered in full from day one

Step 4:Full Coverage

After the waiting period, your policy pays the full benefit amount to your beneficiaries.

Guaranteed Life Insurance Coverage in Canada

Guaranteed life insurance in Canada offers simple, guaranteed approval – but with some important limits.

Coverage amounts are typically smaller:

- Usually between $5,000 and $50,000 (a few insurers do offer coverage up to $100,000 for certain ages)

- Designed to cover final expenses, not large financial needs

Most policies include a 2-year waiting period:

- Full benefit paid after 2 years

- During this time, premiums + interest are refunded (non-accidental death)

- Accidental death is covered from day one

Because approval is guaranteed, costs are higher than policies that require health questions, such as simplified issue life insurance.

You can buy coverage directly or through a broker. A broker can help you compare multiple insurers to find the best rate.

Expert Insight: What to Know About Guaranteed Life Insurance

Watch: Expert explains how guaranteed life insurance works

Guaranteed life insurance offers approval with no medical exams or health questions — but with trade-offs. Coverage is typically lower, premiums are higher, and most policies include a 2-year waiting period.

If you qualify for a plan where you can answer a series of health questions, it will likely result in a lower premium and a better overall plan.

Because options vary between insurers – especially if you have specific health conditions – working with a broker can help you find the best fit for your situation.

Guaranteed Life Insurance by Age in Canada

The cost and availability of guaranteed life insurance in Canada depend heavily on your age.

- Premiums increase with age

- Most insurers have age limits, typically offering coverage between ages 40 and 80

- The older you are, the higher the cost and the fewer options available

People also have different goals depending on their stage in life – from basic protection to covering final expenses.

Guaranteed Life Insurance Under 40

At this age, guaranteed life insurance is usually not the first option, but it can still be useful if you have health issues.

Common reasons:

- You’ve been declined for traditional life insurance

- You want basic coverage without medical exams

- You have serious pre-existing conditions

Sample monthly premiums (Age 35, non-smoker)

| Coverage | Male | Female |

| Guaranteed Life insurance: $10,000 | $16/month | $13/month |

| Guaranteed Life insurance: $25,000 | $34/month | $27/month |

Guaranteed Life Insurance Under 50

More people begin turning to guaranteed coverage due to health changes or past declines.

Common reasons:

- Difficulty qualifying for other policies

- Locking in coverage before rates increase

- Example use: Covering outstanding debts or co-signed loans (e.g., $10,000–$25,000 personal debt)

Sample monthly premiums (Age 45, non-smoker)

| Coverage | Male | Female |

| Guaranteed Life insurance: $10,000 | $22/month | $17/month |

| Guaranteed Life insurance: $25,000 | $48/month | $36/month |

Guaranteed Life Insurance Under 60

This is where guaranteed life insurance becomes more commonly used.

Common reasons:

- Pre-existing health conditions

- Example use: Covering small personal debts, e.g. credit cards (~ $15,000–$25,000)

Sample monthly premiums (Age 55, non-smoker)

| Coverage | Male | Female |

| Guaranteed Life insurance: $10,000 | $34/month | $28/month |

| Guaranteed Life insurance: $25,000 | $78/month | $62/month |

Guaranteed Life Insurance Under 70

Coverage is still available, but costs increase significantly.

Common reasons:

- Avoiding medical underwriting

- Example use: Covering funeral expenses in Canada (~$10,000 – $20,000+)

Sample monthly premiums (Age 65, non-smoker)

| Coverage | Male | Female |

| Guaranteed Life insurance: $10,000 | $70/month | $56/month |

| Guaranteed Life insurance: $25,000 | $152/month | $120/month |

Guaranteed Life Insurance Under Over 70

At this stage, availability becomes more limited and not all insurers offer coverage.

Working with a broker can help you find companies that still accept applicants in this age range.

Common reasons:

- Example use: Covering burial or cremation expenses (~$5,000 – $10,000)

- Leaving a small benefit for loved ones

Sample monthly premiums (Age 75, non-smoker)

| Coverage | Male | Female |

| Guaranteed Life insurance: $10,000 | $135/month | $107/month |

| Guaranteed Life insurance: $25,000 | $334/month | $265/month |

Guaranteed Life Insurance for Seniors and Elderly

For many seniors, guaranteed life insurance is one of the few options available — especially after age 70, when life insurance for seniors becomes more limited and traditional policies are harder to qualify for, e.g.

- Manulife and Canada Protection Plan offer coverage up to age 75

- Assumption Life offers coverage up to age 80

This makes it a practical option if you:

- Have been declined before

- Have pre-existing conditions

- Want coverage specifically for final expenses

Most policies offer coverage up to ~$50,000, with a 2-year waiting period and higher premiums in exchange for guaranteed approval.

For many seniors, it provides peace of mind, knowing their loved ones won’t have to cover funeral or end-of-life costs.

Best Guaranteed Life Insurance in Canada

Most major life insurance companies in Canada offer some form of guaranteed life insurance, along with several specialized providers.

This includes:

- Large insurers like Manulife, Sun Life, and Canada Life

- Mid-size providers such as Assumption Life, CPP, and iA Financial (iA/Ivari)

- Bank-affiliated insurers like BMO Insurance, CIBC, and TD Insurance

However, not all companies offer the same value.

Key differences include:

- Maximum coverage (some cap at $25,000, others offer $50,000+) e.g.

- Manulife offers maximal face value of $100,000 for ages 18-70 and $50,000 for ages 71-75.

- Assumption Life offers maximum coverage of $50,000 for ages 18-75 and $25,000 for ages 76-80

- Canada Protection Plan offers coverages between $10,000 and $50,000 for ages 18-60 and coverages between $5,000 and $50,000 for ages 61-75

- Age limits (some accept applicants up to 75, others up to 80+)

- Pricing differences, which can vary significantly by age

- Policy features, such as partial payouts during the waiting period

You can also explore no medical life insurance options.

Guaranteed Life Insurance Brokers in Canada

We work with experienced brokers who understand guaranteed life insurance and can compare options from over 20 Canadian insurers.

Our brokers help you compare policies and pricing to find the right coverage for your needs and budget.

Insurance Companies We Work With

![]()

Guaranteed Life Insurance vs Simplified vs Traditional

When choosing life insurance, it’s important to understand how guaranteed life insurance compares to other options available in Canada.

The main differences come down to qualification, cost, and speed of approval.

| Type | Medical Exam | Health Questions | Approval Time | Cost |

| 1. Guaranteed Issue Life Insurance | Instant – 24 hours | $$$ | ||

| 2. Simplified Issue Life Insurance | Same day-few days | $$ | ||

| 3. Fully Underwritten Life Insurance | 2 to 6 weeks | $ |

- Guaranteed life insurance offers the easiest approval, but comes with higher costs and lower coverage

- Simplified issue insurance is often a middle ground, with fewer questions and lower premiums

- Traditional life insurance offers the lowest cost, but requires full underwriting

Pros and Cons of Guaranteed Life Insurance

Guaranteed life insurance offers certainty and simplicity, but it comes with trade-offs in cost and coverage.

| Pros | Cons |

| – Guaranteed approval – no risk of being denied | – Higher cost compared to other types of life insurance |

| – No medical exams or health questions | – Lower coverage amounts (typically up to $50,000) |

| – Fast and simple application process | – 2-year waiting period for full benefits |

| – Available for seniors and high-risk applicants | – Limited value if you qualify for other policies |

| – Provides peace of mind for final expenses | – Fewer options at older ages |

Who Should Get Guaranteed Life Insurance?

Guaranteed life insurance is best suited for individuals who may not qualify for other types of coverage but still want a simple, reliable way to protect their loved ones.

This option may be right for you if:

- You have serious health conditions that make approval difficult

- You’ve been declined for life insurance in the past

- You want coverage with no medical exams or health questions

- You are a senior with limited insurance options

- You only need coverage for final expenses (funeral, small debts)

It’s designed for people who value certainty of approval over lower cost.

Who Should NOT Get Guaranteed Life Insurance?

Guaranteed life insurance is not the right choice for everyone, especially if you qualify for more affordable options.

You may want to consider other types of life insurance if:

- You are in good or average health and can qualify for traditional coverage

- You are willing to answer a few health questions (simplified issue)

- You want higher coverage amounts (e.g., income protection or mortgage coverage)

- You are looking for the lowest possible monthly cost

- You are under age 50 and have access to better options

In many cases, simplified or traditional life insurance can offer significantly lower premiums for the same or higher coverage.

FAQ About Guaranteed Life Insurance in Canada

What is Guaranteed Life Insurance?

Guaranteed life insurance is a policy that cannot be declined, regardless of your health. There are no medical exams or health questions, and approval is guaranteed as long as you meet the age requirements.

What is Guaranteed Term Life Insurance?

Guaranteed life insurance is typically whole life insurance, not term. True “guaranteed term” options are rare in Canada. Most guaranteed policies provide lifetime coverage rather than coverage for a fixed term.

What Is Guaranteed Whole Life Insurance?

Guaranteed whole life insurance is a permanent policy with guaranteed approval. It stays in place for life, as long as premiums are paid, and pays a fixed benefit to your beneficiaries.

How Much is Guaranteed Life Insurance?

Costs vary based on age, gender, smoking status, and coverage amount. For example, a $10,000 policy can range from ~$20/month (younger applicants, 45 years old, male, non-smoker) to $70+/month (older applicants, 65 years old, male, non-smoker).

Is Guaranteed Whole Life Insurance worth it?

It can be worth it if you cannot qualify for other types of life insurance. While it’s more expensive, it provides certainty of approval and is often used for final expenses.

Can you have more than one Guaranteed Life Insurance policy?

Yes, you can have multiple policies. However, insurers may limit the total coverage amount, and costs can add up quickly.

Who offers Guaranteed Life Insurance in Canada?

Many insurers in Canada offer guaranteed life insurance, including Manulife, Canada Life, CPP, Assumption Life, and numerous bank-affiliated insurers. Availability varies by age and coverage amount.

How to get Guaranteed Life Insurance?

You can apply online or through a broker. The process is simple:

- Complete a short application

- No medical exam required

- Get approved quickly (often within 24 hours)

What is the waiting period for Guaranteed Life Insurance?

Most policies include a 2-year waiting period. During this time, non-accidental death results in a refund of premiums plus interest, while accidental death is usually covered in full.

What is the maximum Guaranteed Life Insurance coverage?

Coverage is typically between $5,000 and $50,000, depending on the insurer. Some companies may offer slightly higher limits ( e.g. Manulife offers $100,000 for ages 18-70), but this type of policy is mainly designed for final expenses.

Until what age can you get Guaranteed Life Insurance?

Most insurers allow applications between ages 40 and 75, depending on the company. Fewer options are available at older ages (e.g. Assumption Life offers Guaranteed Life Insurance for ages up to 80).