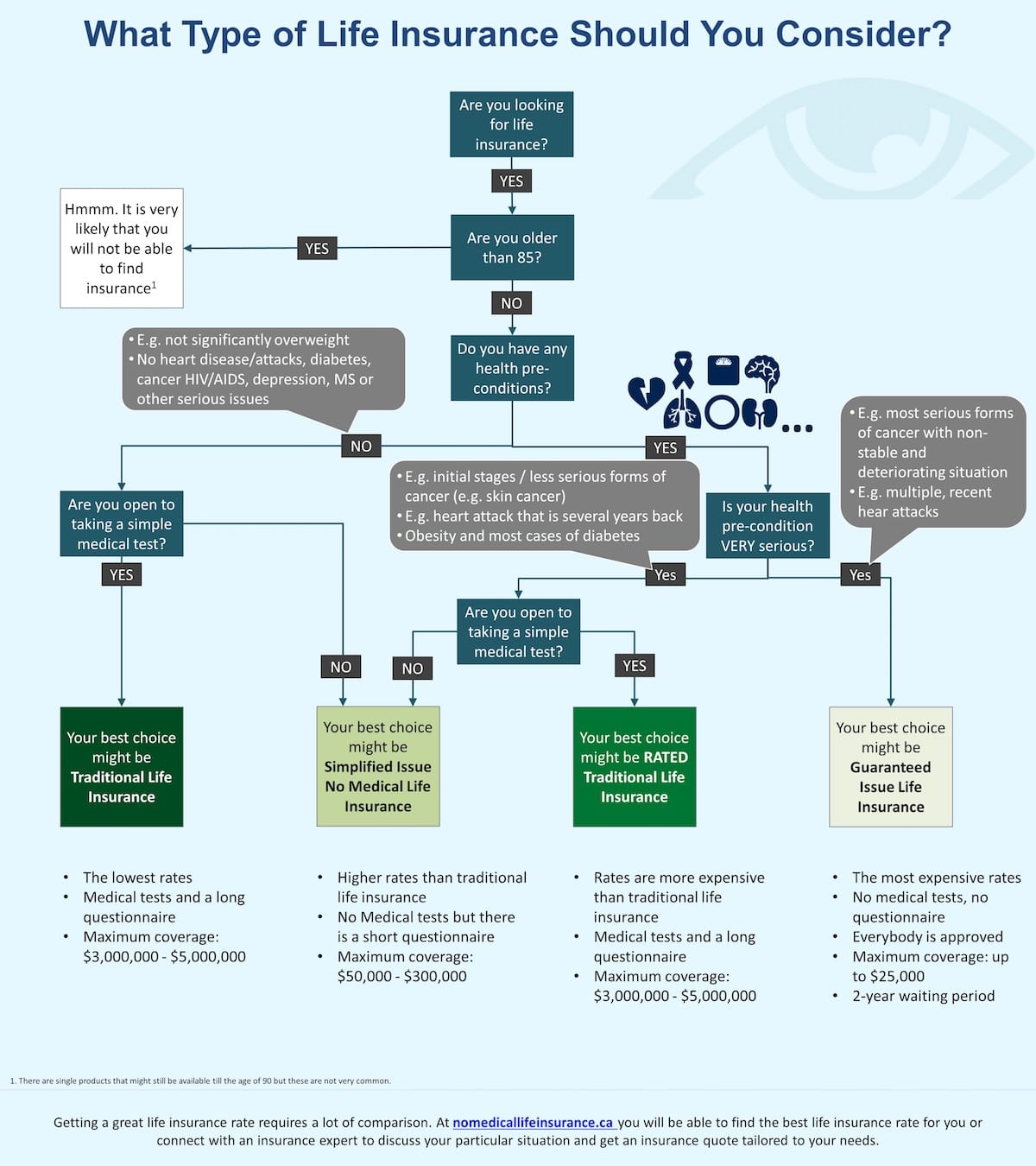

When insurers sell a policy, they always assess risks associated with that policy. Those with lower risks (e.g. younger person, no bad habits, no health pre-conditions) get life insurance rates that are typically lower than those with a history of health pre-conditions and a number of bad habits, like smoking. Based on these risks, you can qualify for one or more of these four insurance types (shown here in order of increasing risk, and thus, increasing coverage costs):

- Traditional Life Insurance (also called Standard Life Insurance)

- Rated Traditional Life Insurance (also called Rated Standard Life Insurance)

- Simplified Issue No Medical Life Insurance

- Guaranteed Issue No Medical Life Insurance

The infographic below shows typical scenarios for each type of insurance, but remember: individual situations may differ – this overview only shows typical cases.

Scenario #1: You have no particular health pre-conditions and you are open to taking medical tests.

In this case, you can benefit from the lowest rates as you be looking into getting a traditional life insurance quote and policy with maximum coverage up to $3-5M.

Example: Term 20 with $200,000 in coverage for a female aged 35 years old will cost around $18/month and $22/month for a male with similar characteristics.

Scenario #2: You have no particular health pre-conditions but you do not want to take medical tests.

You could have benefited from lower rates, but if you do not want to go through the medical exam (it’s common for some people to want to avoid one) you can get simplified issue no medical life insurance. There will be a short questionnaire to complete. Your maximum coverage, however, will be not higher than $300,000.

Scenario #3: You have some pre-existing health conditions which are not too serious and you are open to taking medical tests.

In this case, you would likely qualify for rated traditional life insurance. That means you can still apply for a full coverage of up to $3-5M and still need to pass a medical exam. The only downside is that your premiums will be higher than traditional life insurance.

Scenario #4: You have some pre-existing health conditions that are not too serious, but you do not want to take medical tests.

You could have benefited from traditional life insurance rates, but if you do not want to go through the medical exam, you will be looking at getting a simplified issue no medical policy. There will be only a short questionnaire to complete. Your maximum coverage will be not higher than $300,000.

Scenario #5: You have serious pre-existing health conditions.

In this case, the only choice is to apply for guaranteed issue no medical life insurance. On the positive side, you are always approved since there is no questionnaire to complete and no medical tests to pass. At the same time, your coverage will most likely be limited to $25,000 and there is normally a two-year waiting period on benefits. This means if a policyholder dies within the first two years, no claim will be paid (but the premiums will be returned).

We hope that this overview is helpful as you look into your life insurance choices. Do not forget to use an insurance broker to get a life insurance quote and policy tailored to your particular situation. Our insurance brokers know all the ins and outs of life insurance products from different providers and can recommend the best option.

{kind=link}